The Ultimate Guide for 2023

Welcome to the ultimate guide to the First Home Guarantee Scheme (formerly known as First Home Loan Deposit Scheme) in 2023!

In this comprehensive guide, you’ll discover:

- How to buy a home with just a 5% deposit

- How the expanded scheme will function

- The duration of the First Home Guarantee Scheme

- How you can secure your spot in the First Home Guarantee program right now

And much more! Discover the possibilities of the First Home Guarantee Scheme by diving into this guide today!

What is the Home Guarantee Scheme?

The First Home Guarantee Scheme (FHBG), previously known as the First Home Loan Deposit Scheme (FHLDS), allows the government to act as your guarantor. This means you can purchase a home with only a 5% deposit and avoid paying Lender’s Mortgage Insurance (LMI).

The scheme assists up to 35,000 home buyers each year in purchasing a home with a lower deposit. In previous years, the scheme has been incredibly popular and spots have been filled within months of its release.

There are income and price limits for the scheme that we will discuss below.

Why is the Home Guarantee Scheme beneficial?

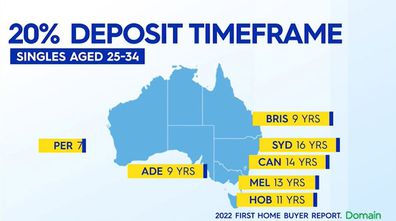

Typically, when buying a home, you would need to save at least 20% of the property’s value to avoid paying Lender’s Mortgage Insurance or rely on a guarantor, such as your parents.

However, with the Home Guarantee Scheme, you only need to contribute 5% of the property’s value as a deposit, with the government (or NHFIC) covering a guarantee over the remaining 15% of the property value. This means you can borrow up to 95% (LVR) of the property value without paying LMI!

By reducing the required deposit to just 5%, the Home Guarantee Scheme allows you to enter the market more quickly and at a lower cost, avoiding the expense of Lender’s Mortgage Insurance.

What are the advantages?

With the government acting as your guarantor, you appear as a lower risk to the bank, enabling you to avoid paying thousands of dollars in LMI and access lower interest rates.

You can enter the property market with only a 5% deposit, compared to the minimum 8% deposit required when paying LMI.

Your weekly payments will go towards paying off your own home loan instead of rent.

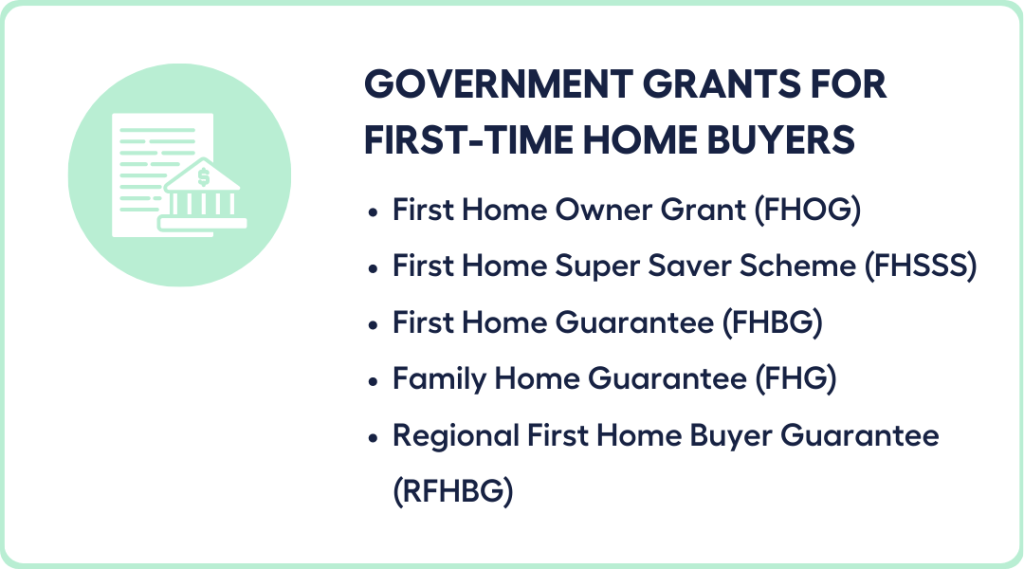

Additionally, you can combine other first home buyer benefits, such as stamp duty concessions, the first home owners grant, and the first home super saving scheme with this new scheme, potentially saving even more.

Speak with your broker to learn how.

What are the disadvantages?

If you purchase with a lower deposit, you will have a higher loan amount and pay more interest compared to borrowing less with a 20% deposit.

The Home Guarantee is limited to 35,000 spots per year and operates on a first come, first served basis. If you’re not quick enough or not prepared, you could miss out.

Some property experts argue that these new schemes may contribute to rising property prices, potentially excluding aspiring home buyers who cannot access the scheme.

The scheme also has a property price cap, which can limit the homes you can purchase as a first-time homebuyer.

How do you know if you are eligible for Home Guarantee Scheme?

We’ve outlined the criteria of the Home Guarantee scheme below.

| Requirement | Eligibility |

| Income | Single applicants: up to $125,000 taxable income for FY23 Couples: up to $200,000 taxable income for FY23 |

| Deposit | At least 5% savings, up to a maximum of 20% savings |

| First Home Buyer | You must not have owned property in Australia in the past 10 years. |

| Citizenship | Australian citizens and Australian permanent residents are eligible. |

| Property Price Cap | Price caps apply; see below |

| Minimum Age | Yes, aged 18 years and older |

| Living Arrangement | You must move in and live in the property as your home within 6 months. If you move out of the home you are no longer covered by the scheme. |

| Relationship | Friends, siblings, and other groups of family members can jointly apply. |

| Banks | Only 27 lenders can offer the scheme, the major banks include CBA and NAB and some non-major lenders include Bendigo Bank, Bank Australia & Teachers Mutual Bank. |

Exciting Updates to the Home Guarantee Scheme for 2023-2024

Starting July 1, 2023, the government is making significant changes to the Home Guarantee Scheme to make it accessible to more home buyers; It’s now:

- available for groups of friends, siblings, and other family members.

- No longer limited to first home buyers – anyone who hasn’t owned property in the last 10 years can apply.

- Available to single legal guardians of children, such as aunts, uncles, or grandparents, who can benefit from the Family Home Guarantee (FHG).

These updates open the door to more Australians achieving their dream of homeownership.

However, with only 35,000 spots available each year, time is of the essence.

To find out if you’re eligible, don’t hesitate to give us a call at 1300 855 244 or complete our free assessment form today.

| Area | Current Price Cap | OLD Price Cap 1st July 2021 to 30 June 2022 |

| New South Wales—capital city and regional centre | $900,000 | $800,000 |

| New South Wales—other | $750,000 | $600,000 |

| Victoria—capital city and regional centre | $800,000 | $700,000 |

| Victoria—other | $650,000 | $500,000 |

| Queensland—capital city and regional centre | $700,000 | $600,000 |

| Queensland—other | $550,000 | $450,000 |

| Western Australia—capital city | $600,000 | $500,000 |

| Western Australia—other | $450,000 | $400,000 |

| South Australia—capital city | $600,000 | $500,000 |

| South Australia—other | $450,000 | $350,000 |

| Tasmania—capital city | $600,000 | $500,000 |

| Tasmania—other | $450,000 | $400,000 |

| Australian Capital Territory | $750,000 | $500,000 |

| Northern Territory | $600,000 | $500,000 |

| Jervis Bay Territory and Norfolk Island | $550,000 | $550,000 |

| Christmas Island and Cocos (Keeling) Islands | $400,000 | $400,000 |

Home Guarantee Property Price Caps

In this section, I’ll provide you with the property requirements for the price caps, including the significant changes that were implemented from 1st July 2022.

If you’ve been struggling with conflicting figures, this guide will be very useful.

What Are the Property Requirements

For the First Home Guarantee (previously the first home loan deposit scheme) both newly constructed and existing homes qualify for the scheme.

How to Apply For the Home Guarantee

In this section, I’ll walk you through the steps to apply and give you insider tips from years of experience helping first-time home buyers.

So if you’re wondering about your eligibility and want to secure your Home Guarantee Spot before they’re all gone, you’ll find lots of valuable information here.

Am I eligible for the First Home Loan Deposit Scheme?

- If you are applying alone, your income has to be max $125,000

- If you are applying with another person, your combined income must be no more than $200,000

- Owner-occupied loans must be set up as (P&I) principal and interest.

What do I need to provide to apply for the First Home Guarantee?

In the first instance, you need to speak with a Mortgage Broker or eligible lender for the reservation process. On top of the regular information you’ll need to provide your mortgage broker, you’ll need:

- Your Medicare Card, and Position on the Card

- Your ATO Notice of Assessment for the taxable year ending 2022-2023

- Regular home loan documents, like your payslips and bank statements.

- Signed First Home Buyer Declaration for FY2023-24

How will my Home Guarantee loan be assessed?

Borrowers will be assessed on the more lenient bank criteria ‘as if’ you had a 20% deposit – in line with their income, loan amount and previous history – like any borrower buying a house.

For your loan to be eligible, you will need to fit the following criteria, including:

- A loan is eligible if the Loan to Value (LVR) ratio is between 80 to 95%

- The value of the property doesn’t exceed the price cap for the area.

- You are applying with one of the 32 lenders that can offer the scheme (ask us which one is best for your circumstances).

- Two borrowers applying must both be eligible as first home buyers or ‘back in the market’ buyers.

- The loan is for a residential property.

- There is a maximum of two borrowers applying, no more.

- The residential property subject to the loan must be owner-occupied.

- The loan term does not exceed 30 years.

What other government schemes can I use in conjunction with the First Home Buyer Scheme?

While you’re applying for the First Home Buyer Scheme, you can use the other First home buyer incentives in combination, like the First Home Super Saver Scheme (FHSS) or First Home Owners Grant (FHOG) towards your deposit!

Do I only need 5% deposit for the Home Guarantee Scheme?

Over and above the minimum required deposit of 5% savings under the scheme, home buyers will need to cover stamp duty, bank fees, legal costs and any ‘out of pocket expenses’.

So for example, a first home buyer in Queensland will need at least $30,000 (5%) deposit on a $600,000 purchase plus extra deposit funds to cover the costs, which include:

- Stamp Duty – $12,850

- Transfer Duty – $1751

- Government Fees – $197

- Bank fees – $700 (establishment fees, valuation fees which range from $0 to $700)

- Conveyancing Fees – $2,000

- Building/Pest Fees – $500

- Lenders Mortgage Insurance – $0 waived under Home Guarantee Scheme

On top of the 5% savings of $30,000 you’d need a further $18,098 to cover these costs bringing your total deposit to $48,098.

How much LMI am I saving with this scheme?

LMI is calculated on a sliding scale, so the actual savings will vary depending on the deposit you put in and the loan to value ratio (LVR) and your homeloan amount.

| Deposit Option | LVR | LMI Costs |

| 1. Lowest Deposit | 95% inc LMI | $26,471 |

| 2. 10% deposit | 90% + LMI | $15,267 |

| 3. 12% deposit | 88% + LMI | $10,537 |

| 4. 20% deposit | 80% | Nil |

For example, If a home buyer purchased in Brisbane for $700,000 without access to the FHBG, they would have to pay the following LMI – see table below

With the FHBG, the LMI they would have to pay is ZERO which is a massive saving

How long the Home Guarantee Scheme will last?

It’s difficult to say how long the placements for the Home Guarantee Schemes will last, as it is on a first-come, first-served basis so if you want to secure a spot today contact our Mortgage Brokers.

Next Steps

I hope you enjoyed this updated guide to the First Home Buyer Guarantee Scheme in 2023.

If you’d like help with applying for your Home Guarantee Scheme and securing a home, leave a quick message here and our Mortgage Brokers will be in touch shortly.