The royal commission and a tougher regulatory environment for the banks in 2018 translated to stricter borrowing conditions for borrowers, and a less competitive market than years gone past.

The royal commission and a tougher regulatory environment for the banks in 2018 translated to stricter borrowing conditions for borrowers, and a less competitive market than years gone past.

This environment will carry into the rest of 2019 with more stringent loan assessments from lenders. This is made easy for them by the spending and saving behaviours of borrowers being increasingly online and electronic.

In short: Australians are living their lives online, and it’s easier for lenders to get a full picture of how they manage their money.

Borrowers have “nowhere to hide” when it comes to their spending habits, and should be aware their discretionary spends are on lenders’ radars.

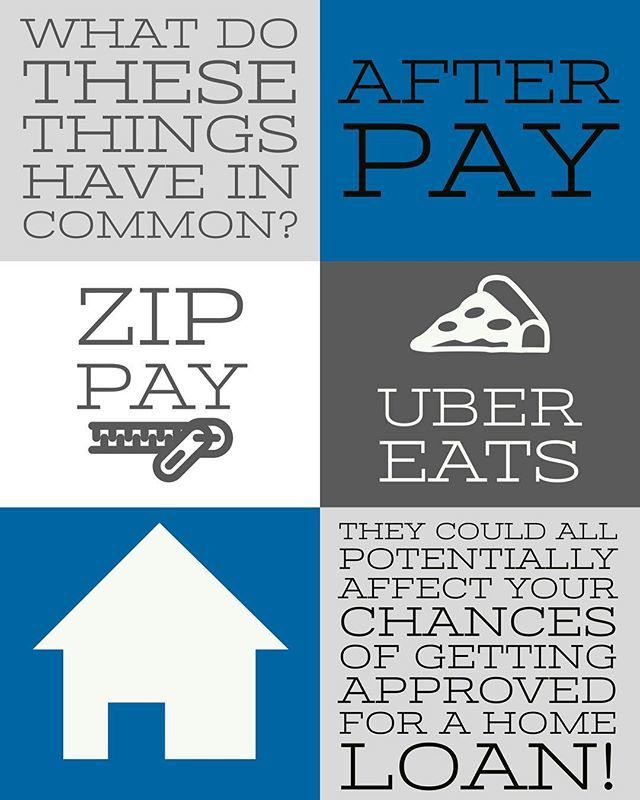

Most banks now require transaction statements, which means borrowers can’t hide with their history of spending. The rise in ‘tap and go’ payments plus technology such as bankstatements.com.au can classify spending into categories and give a lender full visibility on a loan applicant’s spending patterns and how much they save – this level of disclosure is unprecedented.

Examples include Afterpay, Zip Pay, frequent holidays, high spending on credit cards and even spending on gambling, alcohol and dining are being hauled into question if they will be ongoing expenses after their loan has settled or if this constitutes discretionary spending.

Getting ahead

There are steps borrowers can take to make themselves a more attractive candidate including the tried-and-tested drawing up a budget and reducing liabilities.

Most borrowers can’t provide a budget, so this is a great place to start. Get your spending under control and show the bank you have a track record of saving to demonstrate confidence you can repay a loan. Get rid of credit cards you’re not using or reduce limits, it helps to improve borrowing capacity, and clear Zip Pay or Afterpay purchases… Get rid of them.

Most importantly is your ‘conduct’ on your current loans – if you are showing missed or late payments this could be a deal breaker for some banks. Also pick your lender wisely. For example, applying to Westpac means they can look through your account conduct if you have St George accounts as St George is owned by Westpac. (Like Bankwest is owned by the Commonwealth Bank)

Why loans get knocked back

Some common characteristics in mortgage applications that lenders knock back are

– Spending habits, particularly via popular new payment platforms, made the list.

– Lenders are now going through individual bank statements “with a fine tooth comb” which can shed light on excessive retail spending or out-of-budget impulse purchases.

– If a borrower is an eBay enthusiast, Afterpay addict or has an excessive number of entertainment subscriptions, they might be in trouble.

Whether you are looking to buy your first home, move home, refinance, or invest in property, a mortgage broker can help. Access loans from all the major lenders, get help with paperwork – plus there is no charge for this service.

Get help from your Go Mortgage broker – Call NOW